Harvesting value: How to price Saas and other products better

The American Marketing Association defines marketing as:

the activity, set of institutions, and processes for creating, communicating, delivering, and exchanging offerings that have value for customers, clients, partners, and society at large.

Marketing is about communicating value. Products and offerings deliver that value. So how does a company harvest value?

Pricing.

According to Mark Bergen, marketing professor at the Carlson School of Management, pricing is:

[T]he moment of truth. It's where all of our marketing strategy really meets that final decision point with our customers.

The four levers of profit and why price is important

Businesses operate to generate value, revenue, and profit. Price is one of the four levers a company can pull to increase profitability:

- Sales

- Variable costs

- Fixed costs

- Price

Increasing ad spend to grow market share pulls the sales lever. Cost reductions tug on the variable costs lever. Reducing leased office space pulls the fixed cost lever. Increasing (or decreasing) how much a product is sold for is the price lever.

Price is the last lever many companies pull because it's the scariest, most public facing of the bunch. But the price lever is also the most efficient way to increase (or decrease) profitability.

Why pull any lever? Profitability.

In their book Smart Pricing: How Google, Priceline, and Leading Businesses Use Pricing Innovation for Profitability, Jagmohan Raju and Z. Zhang conclude that each lever effects profits differently.

- A 1% increase is sales --> +3.3% profitability

- A 1% reduction in fixed costs --> +2.5% profitability

- A 1% decrease in variable costs --> +6.5% profitability

- A 1% increase in price --> +10.3% profitability

If this is true, why don't more people pull the price lever?

Because, according to Raju and Zhang, price carries the most perceived risk. Price directly impacts consumers and can change the way they perceive a product. "Companies willing to pull the price lever face more promise than risk," say the authors, and they advocate for a studied approach to price changes.

How to set our price

Not all pricing methods are created equal. The pricing approaches we'll cover here are:

- Cost-plus pricing

- Competition-based pricing

- Consumer-based pricing

- Value-based pricing

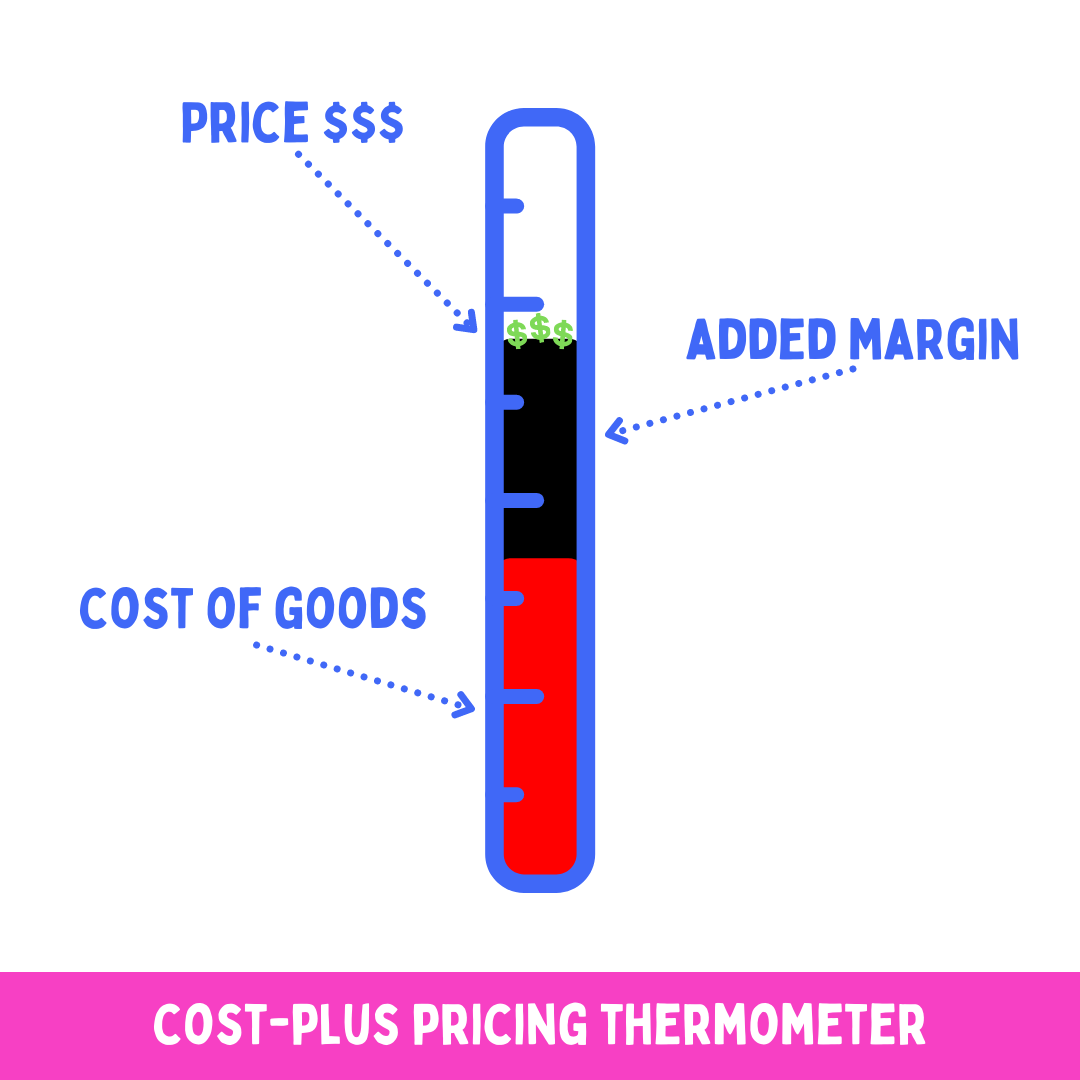

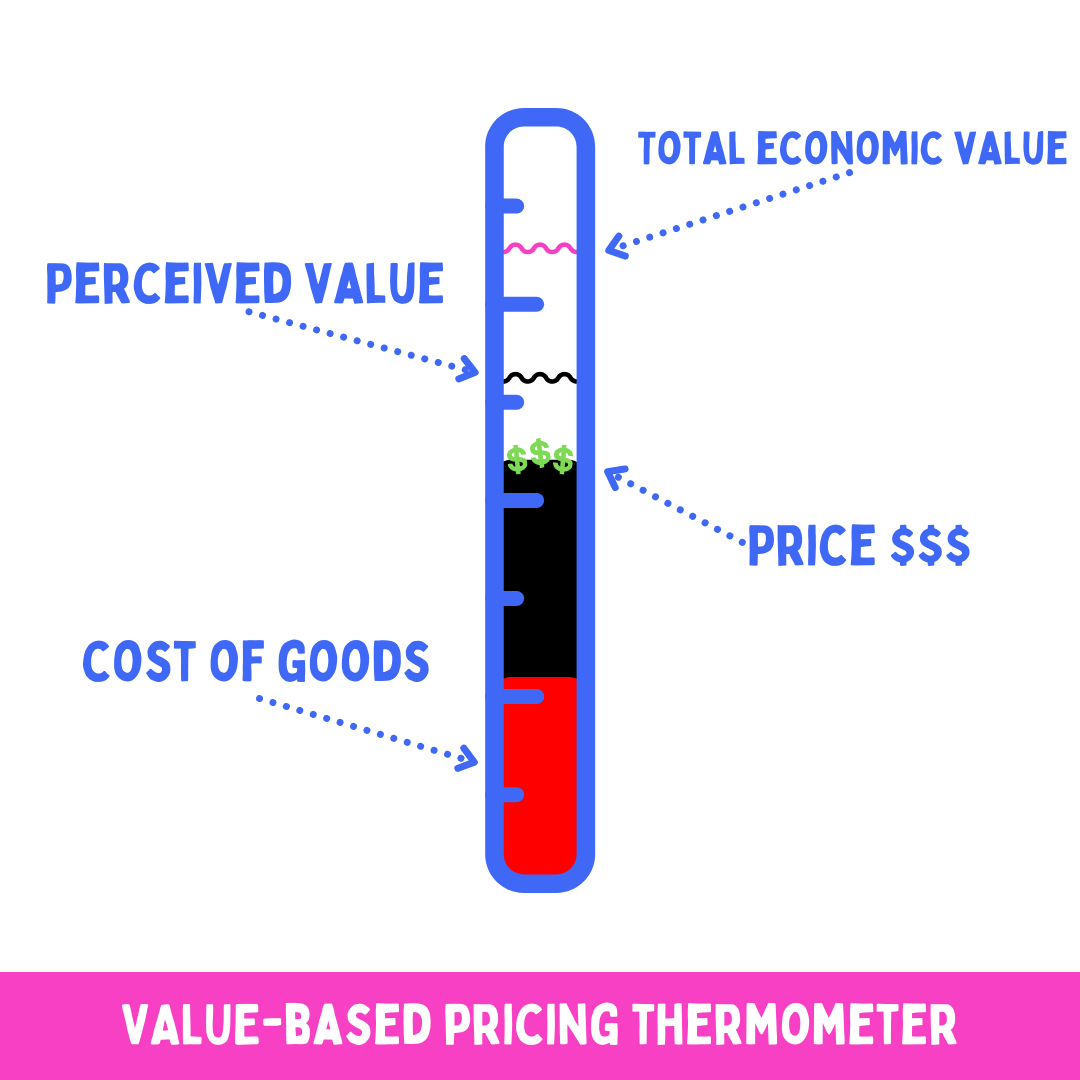

Using a pricing thermometer like the one shown below, let's look at how each approach gets us to a price.

Cost-plus pricing

For Cost-Plus Pricing we start at the bottom of the thermometer with the Cost of Goods Sold (COGS). COGS is the sum of the direct costs of producing goods sold by our company. We can also include indirect costs such as marketing, staff, warehousing, and other overheads.

Then we add a markup or margin that gives us room to pay for our costs while leaving money left over for profit. Cost-plus pricing is simple if we know our costs.

There are a few problems with cost-plus pricing, though.

- It's hard to know exactly how much each unit actually costs

- Cost-plus pricing ignores the market and focuses only on us and our product

Cost-plus pricing doesn't account for how much value different customers get from the product. We're probably underpricing and leaving money on the table. That's no good.

Competition-based pricing

Competition-based pricing is calculated by checking competitor pricing and setting our price relative to that.

There isn't much research needed, so it's easy to make pricing decisions like this. Simply figure out what everyone else is charging and put our prices up or down a little to stay within the same range.

There are two problems with this pricing approach.

- Focusing on what everyone else is charging takes our focus off our customers and our business

- Competitors might figure out what we're doing and cut prices to gain market share

Competitors may have entirely different cost structures, marketing strategies, and who-knows-what that doesn't align with how we run our business. We probably don't know enough about how the competition runs, so we might also be playing a game of high-stakes chicken.

If our price is lower and our products are similar, sure we might gain sales and market share. But this game is a race to the bottom that often leads to disaster.

By focusing on the competition we can lose sight of our company's well-being. Price cuts can leave us with no money to operate with if we start selling our products at a loss just to win market share competitors. Don't do that.

Consumer-based pricing

This is the familiar car yard pricing model. Consumer-based pricing is about figuring out what an individual is willing to pay. Some people may perceive our products as more valuable -- those people pay more. Others may not value our product as much -- these people pay less.

This is a complicated approach to pricing that can lead to some sticky situations. For example, when you take a car out for a test spin, the conversation you have with the sales person is them feeling you out. They're seeing if you're going to negotiate and for how much. Meanwhile, you know the price you pay depends on how well you negotiate, so you pretend to not like the car. You're playing a game and trying not to lose.

It sucks to learn a friend bought the same car for thousands less.

Flipping it around, there are lots of car yards who compete against each other. It's easy for buyers to shop around and play one dealer off another. This usually means nobody ends up truly happy with the price.

Value-based pricing

This is the most market-oriented approach and the hardest to figure out. It also offers the most upside.

Value-based pricing still uses COGS, but treats it as the absolute minimum that can be charged for a product. From there, we look to the top of the thermometer and attempt to work out the Total Economic Value (TEV; aka Objective Value) of the product to buyers. Total Economic Value is summed up like this:

TEV = Cost of the Next-best Alternative + Value of Performance Differential

I struggled turning the formula into words, but here goes:

Total Economic Value is the cost of a similar product plus how much more effective my product is at solving the same problem

Next, we have to determine how customers perceive the value of the product (Perceived Value). This number should equal the highest price consumers are willing to pay for our product.

But how do we figure out what customers are willing to pay?

- Surveys give a broad view of the market, but are based on a hypothetical willingness to pay and people are bad judges of their future behavior (aka, we lie when asked questions like this)

- Interviews reach fewer people but are based on actual purchases and prices people have already paid

A combination of surveys and interviews should help set a Perceived Value.

Value-based pricing is almost entirely focused on customers and the market. It provides the most value to customers and harvests as much value (profit) as as possible. Prices should match Perceived Value. Everybody wins. This is good.

Why value-based pricing is exciting

Value-based pricing shows a true measure of two things:

- The gap between Perceived Value and Total Economic Value is a measure of marketing competency

- The gap between Product Price and Perceived Value is a measure of pricing competency

Marketing and pricing are critical skills for any business. What's exciting is that both skills can be learned and practiced, so even if we don't feel confident in our marketing and pricing skills right now, we can get better through practice and even hiring.

Stop #&$% discounting and pricing yourself out of existence

Discounting and underpricing activate sales by charging consumers less. But both are s#!7 for business.

Underpricing = A slow death

Consulting firm McKinsey claims 80-90% of prices are too low. If we don't set price based on rigorous methods like value-based pricing we're probably leaving money in the market. Lots of money. And leaving money in the market sucks and is dangerous.

Underpricing leads to reduced revenues and smaller profit margins. Brand perception is undermined by low prices because people generally associate lower price with lower quality. Brand perception is a long-term play and the impacts of lowered brand perception might be slow to hit, but it'll hurt when they do.

Lower suggested retail pricing can lead to smaller margins for distributors and retailers, which could make them think twice about stocking our products.

Less profit means less marketing investment and support for our brand. Can you see how underpricing spirals out of control?

Dangerously low prices can put us in the unenviable position of having to fight hard to convince the market that our products are worth more.

Note: Sustainably low prices are fine. Low prices aren't the problem. Prices that are so low we lose money on every sale, that's the problem.

The danger of discounting

Research suggests that for every 1% we discount a product we can hurt profitability by up to 40%.

Read that again.

For every $1 discounted, we can lose $40 in profits? That's ridiculous. Even if that's half true, discounting loses lots of money. And it's not the only bad thing that happens when we discount.

Price-based promotions and discounts eat away brand equity and our product can turn into a commodity. Being a commodity means we're the same as everyone else and the only way to compete is on price. That's not good.

Elon Musk refuses to discount Teslas and I love him for it. Car shopping sucks. Haggling is tiresome and leaves us feeling like we A) got a great deal, or B) we're suckers who paid too much. Tesla sells cars at the same price to everyone, because it sucks to be the guy who paid an extra $10,000 for the same car a neighbor drives. This is why Elon thinks discounting is shitty:

The acid test is that if you can't explain to a customer who paid full price why another customer didn't without being embarrassed, then it is not right. We either win in a way that is fair and right or we lose with our honor intact and accept the consequences. Elon Musk in a message to Tesla employees

How cool is it to be in business to fight fair and lose honorably? I don't want to lose, but let's reframe that a bit:

Not every customer is a good fit for our brand and it's a win for everyone when, for the right reasons, a sale is not made.

Discounting also signals low confidence in the value of our product. This has a direct impact on consumers and channel partners. If we back our product and understand its value to consumers, discounting doesn't need to happen.

So, why this fuss about pricing?

Price is the one lever we can pull that has an immediate and outsize impact on our profitability. Small pricing changes can add real value back into our businesses because price is how we harvest what we've sowed.

The formula is simple really:

Value in > Value out

Build as much value into your product as possible so your prices let you harvest massive value from the market.

Five things to remember when reviewing pricing

- Price may be the least used lever, but smart pricing can add immediate and massive value back into our business.

- Low prices are only dangerous when they're unsustainable. Underpricing and discounting can have massive, long-term negative impacts on the health of our businesses.

- Figuring out what the market perceives our products to be worth is how we harvest the most value. Work hard to figure out a value-based pricing strategy.

- Pricing is a skill that can be improved with practice, so don't expect to get it right every time, but do keep learning and working at it.

- Win and lose with honor. Pricing should be fair, equitable, and the same for everyone.

This is the first post in a series on marketing. Here's a full list of the other posts. I'll update each one with links as soon as they're published.

- How epic companies like Nike and Amazon grab advantage with market orientation

- How to do market research for a startup (from a Saas product marketer)

- Market segmentation? Unwrap the best way to nail your marketing strategy

- Your next market targeting strategy must highlight these two things

- What is market positioning and where does it fit into your marketing strategy?

- The 4 laws of marketing objectives that will inspire your team

- How to build successful products your customers want to buy

- Integrated Marketing Communications (coming)

- Distribution (coming)